Fintech perspectives from a bunch of policy wonks. The views expressed herein are those of the authors and should not be attributed to the Bank for International Settlements or the International Monetary Fund

Author: kiffmeister

The Kiffmeister is a former Senior Financial Sector Expert at the International Monetary Fund.

The US-based Bank Policy Institute (BPI) is raising concerns that a sizeable proportion of Circle’s USDC stablecoin reserves could be parked at the Federal Reserve, despite Circle not having a central bank account. Since November, BlackRock has been managing about two-thirds of the reserve assets in a bespoke money market fund, the Circle Reserve Fund (CRF) , which invests mostly in U.S. short-dated Treasuries. The BPI claims that Blackrock has applied for the fund to access the Fed’s overnight reverse repo (ON RRP) facility, which provides money funds and government-sponsored enterprises a standing option to invest overnight with the Fed at a fixed rate, currently 4.3%. This involves the fund buying Treasuries from the Fed, which are resold to the Fed at a future date at a slightly higher price. The net effect of the cash flows, with the transfer of money to the Fed, is not dissimilar to depositing the USDC reserve cash at the Federal Reserve. The use of the ON RRP by the CRF could effectively transform USDC into a “backdoor” synthetic central bank digital currency (CBDC) if all of the assets are parked there. [Read more at the BPI]

However, Ledger Insights points out there are some frictions and applications to the application process that might trip up BlackRock’s purported ON RRP application on behalf of the CRF. First off, applicants must have been operating for at least one year, and the CRF was launched in November 2022 so the earliest it could apply would be in November 2023. Also, the application form asks about the proportion of shareholders in high risk sectors from an anti-money laundering (AML) perspective. Given Circle is the sole shareholder and its involvement in the cryptocurrency and DeFi sectors, that would be 100%. Nevertheless, the BPI fears that if and when the CRF gets Fed ON RRP access, USDC would become equivalent to an account at the Fed and a “breathtaking example of regulatory arbitrage… and introduce the potential for systemic contagion from the crypto markets into the traditional financial system.” However, IMF and New York Fed staff have written rather positively about the possibility of stablecoins backed directly by central bank deposits, although the Fed has been reluctant to give Master Account access to non-depository institutions, and even banks, like Wyoming-chartered Custodia Bank.

Interestingly, the Fed covered this in an appendix to a 2022 paper on the Macroeconomic Implications of CBDC that is well worth reading (see below). It concludes that, “while research has shown that take- up in the ON RRP can crowd out private repo, and that the demand for safe assets can increase ON RRP take-up at the expense of private repo, the overall impact on the banking sector so far has not led to a significant contraction in bank deposits or bank lending… That said, the effect on the banking sector could change as short-term interest rates increase and the Federal Reserve’s balance sheet contracts.”

The Sovereign Yidindji Government launched a digital version of their Sovereign Yidindji Dollar (SYD) on January 26, 2022, and the first successful transaction was confirmed on February 1. The new payment system is connected to the MetaMUIself-sovereign identity system that is already in use throughout Yidindji. The Sovereign Yidindji Government and MetaMUI are calling the SYD a central bank digital currency (CBDC) and the purpose of this post is to ascertain the “CBDCness” of the SYD.

Yidindji is an Australian pre-colonial indigenous nation that asserted its independence and continuing validity of Yidindji laws and customs in 2014, in accord with Resolution 1514 adopted by the United Nations General Assembly in 1960. However, until a treaty is signed between the governments of the Commonwealth of Australia and the Sovereign Yidindji Government, regarding land rights, Yidindji will not be represented by the United Nations or international law.

Is the SYD a central bank digital currency?

According to the Bank for International Settlements (BIS) a CBDC is a digital payment instrument, denominated in the jurisdiction’s unit of account, that is issued by and a direct liability of the jurisdiction’s central bank or monetary authority. The SYD is a obviously a digital payment instrument, and the rest of this note argues that it seems to meet the other BIS CBDC criteria too.

Does the Yidindji Nation have a central bank?

The Yidindji Reserve Bank Act 2016 established the Yidindji Reserve Bank (YRB) as the central bank of the Yidindji Nation to issue SYD. The SYD was pegged to the Australian Dollar (AUD) and backed by gold and silver.[1] The Yidindji Department of the Treasury guarantees the ability to exchange from SYD to AUD. Appropriate amounts of AUD are held by the YRB to for these exchanges. (Before the introduction of the digital currency, SYD transactions were settled in commercial bank money on a manual ledger.)

However, according to the Act, the YRB wasn’t responsible for some of the key functions associated with a central bank. The YRB had no payment system role, and it was prohibited from issuing bearer money, both foundational central bank roles. But the Act was revised in 2022 to give the YRB typical central bank responsibilities, including issuing currency, regulating/supervising deposit-taking institutions, and overseeing and promoting an efficient, sound, and safe payment system. So, Yidindji has a central bank.

Is the SYD denominated in the Yidindji’s unit of account?

To be a unit of account, a currency must be usable as a medium of exchange across a variety of transactions between several people and as such represent a form of co-ordination across society. The Yidindji Currency Acts of 2014 and 2022, Yidindji citizens must settle their obligations in SYD, and Australian citizens must settle their obligations in AUD.[2] But the two currencies are convertible one-to-one, it would seem that, if the digital SYD is convertible one-to-one into SYD and AUD, which are both units of account in Yidindji, then there’s no reason to dispute its status as a unit of account.

Conclusion

When Yidindji’s central bank is fully operational and carrying out typical central bank operations and responsibilities, the digital SYD will indeed be a CBDC, as it will meet all other CBDC defining criteria; like being issued and backed by, and a direct liability of, Yidindji’s central bank, and being denominated in Yidindji’s unit of account.

[1] Gold and silver bars are kept in two undisclosed locations. These bars are from internationally recognized mints and meets current standards of fineness, majority are from Perth Mint with much smaller amounts from other mints. All bars are in accord with the specifications of the LBMA Good Delivery Rules though not listed on the LBMA list. Once again it is this lack of formal agreement to be seen legally in the UN sphere of jurisdiction. The gold is rebalanced on a monthly basis, whilst audits of the metals take place at three monthly intervals.

[2] Upon the completion of a treaty with the Commonwealth of Australia, the SYD will be the only mechanism for Yidindji residents to discharge their monetary obligations.

One of the first big retail central bank digital currency (CBDC) design decisions is the operating model. In a single-tier model the central bank performs all the tasks involved, from issuing and distributing the CBDC to running user wallets. In multi-tier models, the central bank issues and redeems CBDC, but distribution and payment services would be delegated to the private sector. Which model to adopt will depend on country-specific circumstances, such as financial sector breadth and depth, financial integrity standards compliance, and financial market infrastructure availability and supervision capacity.

Single-tier models

In a single-tier model, CBDC transactions resemble transactions with commercial banks, except accounts would be held with the central bank. A payer would log in to an account at the central bank through a web or mobile application and request a transfer of funds to a recipient’s account, also at the central bank. The central bank would ensure settlement by updating a master ledger, but only after verification of the payer’s authority to use the account, enough funds, and authenticity of the payee’s account. This mode gives central banks more control over the product design and implementation process.

However, the single-tier model requires the central bank to assume an active role in distribution and payment services that may exceed the scope of its core mandate and capacity. Moreover, central banks would directly compete with existing digital payment service providers creating disintermediation risk. Conceptually, the single-tier model may be appropriate for a country with a well-resourced central bank in which the financial sector is extremely underdeveloped, so that there are no institutions to assume distribution and provision of payment services, as may be the case in some low-income countries.

Multi-tier models

In multi-tier models, the central bank issues CBDC but outsources some or all the work of administering the accounts and payment services. However, CBDC remains the liability of the central bank and thus CBDC holders would not be exposed to default risk of the engaged payment service providers (PSPs).

The multi-tier model has been the overwhelmingly preferred solution in CBDC pilots and the only launch so far. Running currency distribution is not something the central bank is well-suited to perform, requiring customer-facing activities that may be beyond their capacity. Also, the multi-tier model is less disruptive than the single-tier one as financial institutions play their traditional roles in distribution and payment services. In addition, this layered approach facilitates the integration of new types of consumer electronic devices without the need to alter the core of the system, and it supports the ability for third parties to build on top of the core (Shah and others, 2020; Armelius et al, 2021).

Different Flavors of Multi-Tier

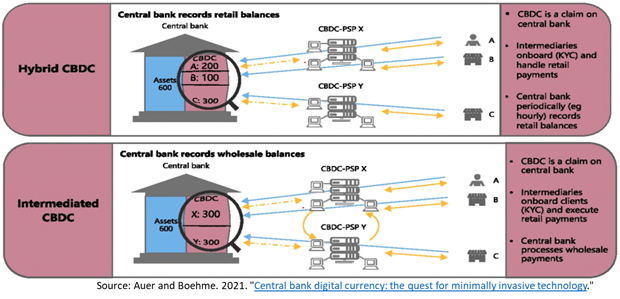

Auer and Boehme (2021) discuss two different multi-tier models that differ in terms of the records kept by the central bank. In a “hybrid” architecture the central bank records all retail CBDC holdings and the CBDC is never on PSP balance sheets so that user holdings are not exposed to claims by PSP creditors in the event of PSP insolvency (first panel below).

In an “intermediated” architecture the central bank only runs a ledger of PSP wholesale CBDC holdings (second panel). Central banks may prefer this architecture due to privacy and data security concerns. However, the central bank still must honor CBDC holder claims in the event of PSP insolvency or data breaches, relying on the integrity and availability of the PSP’s records. This will require close supervision to ensure that the wholesale holdings add up to the sum of all retail accounts at all times.

Auer and Böhme (2020) suggest that, in an intermediated architecture, there be a legal framework that keeps user CBDC holdings segregated from PSP balance sheets so that the holdings are not considered part of a failed PSP’s estate available to creditors. They also suggest that the legal framework could give the central bank the power to switch user accounts in bulk from a failed PSP to a functional one. To do this expeditiously, the central bank would likely have to retain a copy of all retail CBDC holdings.

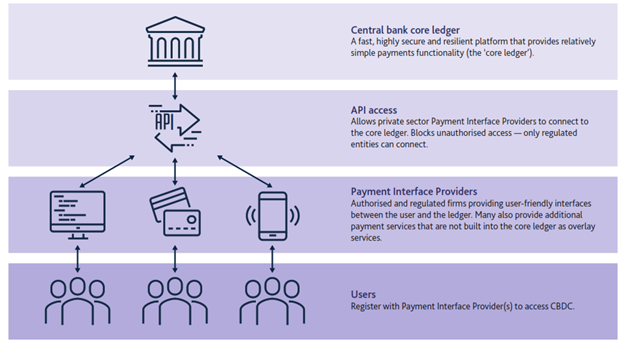

Bank of England (2020) proposes running a hybrid architecture on a “platform” in which the central bank provides a fast, highly secure and resilient technology infrastructure to provide the minimum necessary functionality for CBDC payments (the “core ledger” below). Payment interface providers would connect to it via an application programming interface (API) to provide customer facing CBDC payment services. This model effectively “combines indirect connection to the central bank with direct access to the central bank balance sheet and the CBDCs.” (Prates, 2020)

Overarching Multi-Tier Model Considerations

The multi-tier CBDC ecosystem should be designed to create economic incentives for PSPs to participate in ways that serve central bank interests (making the CBDC broadly available to the public, across regions, etc.). There should be a cost-effective business model for such PSPs with enough revenues from interest spreads, fees, and cross-subsidization, as well as controllable fixed and variable costs. Also, regulations should leave room for enough users to reach critical mass and incentivize network buildup while promoting PSP market competition.

For example, regulations that encourage interoperability of competing payment systems to encourage new entrants and reduce concentration risk should take care not to adversely impact network build-up. (For a new PSP, interoperability across PSPs could diminish the incentive of a startup to innovate since it could lower the value of a privately developed network. It could also restrict competition by excluding certain technical innovations or restricting new business models and reduce the value and increase the costs to PSPs. In addition, interoperability might increase overall risks if an innovative service provider has a higher risk profile.)

Central banks that have made the decision to explore retail central bank digital currency (CBDC) issuance are focusing on a common set of key design choices. These include the operating model, the technology platform (centralized versus decentralized database technology, or token-based), degree of anonymity/privacy, availability/limitations, and whether to pay interest. These design decisions are driven by country-specific factors and balance the need to achieve the policy objectives that launched the exploration process and be attractive to users and merchants. (For more detail on these factors and considerations see the 2020 IMF working paper on CBDC operational considerations.)

In this blog I want to talk about the technology platform decision, broadly speaking breaking down into those with centralized or decentralized ledger architectures, and ledger-less offline peer-to-peer stored value platforms. In a traditional centralized ledger (client-server model with no distributed components) transaction processing would entail the payor connecting to the central ledger keeper and initiating a funds transfer to the recipient’s account. The ledger would be updated after the payor has been confirmed as the account holder who has enough funds to carry out the transaction.

Alternatively, the ledger could be run on a distributed ledger technology (DLT) platform, in which the ledger is replicated and shared across several participants. With a DLT platform the central bank could have a centralized, decentralized or partially-decentralized authority for verifying and/or committing transactions. DLT platforms can be “public” (accessible by anyone) or restricted to a group of selected participants (“consortium” or “private”). Ledger integrity can be managed by a selected group of users (“permissioned”) or by all network participants (“permissionless”).

So far, central banks that have reached the proof of concept (PoC) and pilot stages of CBDC explorations have opted platforms that allow for control over platform access and participants, and role-based oversight and visibility of transactions (see table). Such platforms also ensure that the central bank retains full control over money issuance and monetary policy. They include centralized ledger and DLT private permissioned platforms, and digital bearer instrument platforms. Permissionless (decentralized authority) platforms have tended to fall short on scalability, and settlement finality, and financial integrity risk management.

It has been generally believed that centralized platforms process transactions more quickly. VISA says their network can handle up to 65,000 transactions per second (TPS), while private DLT platforms have tended to be way slower (e.g., 10,000+ TPS). There is also the issue of “finality” – the point at which transferred funds become irrevocable. Some networks, like Bitcoin and R3 Corda, offer only what is called “probabilistic finality” which won’t cut it for a retail payment system.

Although all the pros and cons of DLT-based versus centralized ledger-based retail payment systems are out of scope of this post, it’s worth mentioning that DLT-based platforms may offer enhanced resiliency by reducing single points of failure. Also, potential data loss at one node can be recovered through replication of the ledger from other nodes when the network comes back online. But DLT-based platforms may experience attacks against the network layer, which includes the consensus mechanism by which database updates are approved, or smart contract exploits. (For more on such pros and cons, see Raphael Auer and Rainer Böhme’s Technology of Retail Central Bank Digital Currency article)

In the table below, I’ve listed what I believe to be the main players in the retail CBDC platform space. My main criterion for inclusion is that the platform has been used in a CBDC or sovereign digital currency pilot or proof of concept or has published something substantive to back up the claim that it offers a viable CBDC platform. I’ve tried to categorize them by whether they’re ledger- or token-based, and if they’re ledger-based, whether the ledger management is centralized or distributed. My plan is to make this a “live” table, and possibly add more columns based on your comments and suggestions. If you have platform suggestions that I’ve missed, please provide links to written material that supports the claim.

In a previous post I discussed what is and isn’t a retail central bank digital currency (rCBDC): A broadly available general purpose digital payment instrument, denominated in the jurisdiction’s unit of account, that is a direct liability of the jurisdiction’s monetary authority, and subject to the same rules and regulations as imposed on the jurisdiction’s other units of account. The gist of this is summarized in the following table.

I then went on to describe wholesale central bank digital currency (wCBDC) as being like an rCBDC, but being restricted to wholesale, financial market payments. But some will notice that I never mentioned the technology platform – whether it runs on a centralized or decentralized ledger, or whether there is even a ledger at all (i.e., “token” based). And that’s because discussions around rCBDC are generally agnostic about the platform type. However, it’s my sense that that is not the case for wCBDC.

And that may be because wCBDC is not really anything new. For example, a 2018 IMF staff discussion note characterized central bank reserves as a “wholesale form of CBDC used exclusively for interbank payments” which has been around for ages. And in 2020, ECB legal staff noted that “the issuance by central banks of digital liabilities and the corresponding holding, by third parties, of intangible money claims against the balance sheet of the digital liability-issuing central bank would not represent a genuine novelty.”

And a 2020 paper that surveyed wCBDC research found that “the overarching motivation for CBDC research by CBs is to assess the impact of distributed ledger technology (DLT) on financial market infrastructures (FMIs). Which all implies to me that when people say “wholesale CBDC” they really mean to say is “distributed ledger technology (DLT) based wholesale CBDC. This may be a trivial discussion but when we say “retail CBDC” we encompass all platforms (centralized, distributed and token-based) and as everyone knows I’m a stickler on definitions!

And although I don’t follow wholesale CBDC developments closely, I’ve tabulated below the experiments that have popped up in my Daily Digest. If I’ve missed any, please let me know in the comments! FYI I plan to keep the table updated on my Kiffmeister Chronicles blog. That’s also the best version of the table to use if you want to follow the live links in the “references” section.

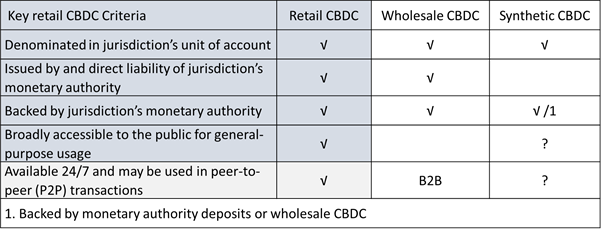

According to the Bank for International Settlements (BIS), a retail central bank digital currency (CBDC) is a broadly available general purpose digital payment instrument, denominated in the jurisdiction’s unit of account, that is a direct liability of the jurisdiction’s monetary authority. To this I would add, subject to the same rules and regulations as imposed on the jurisdiction’s other units of account. By “general purpose” is meant that it can be used by the public, for day-to-day payments rather than CBDCs restricted to wholesale, financial market payments. A liability issued by a monetary authority that is not in its own currency (i.e., where it does not have monetary authority) is not a CBDC. I’ve summarized this definition in the table below and have added that it can be used for peer-to-peer transactions, which the Banque de France also views as an essential characteristic.

In previous versions of this tabulation, I included legal tender status as a key characteristic. A currency’s legal tender status entitles a debtor to discharge monetary obligations by tendering the currency to the creditor. However, a recent IMF working paper casts doubts on whether a digital currency can, or even should be given legal tender status. For example, designating CBDC as legal tender is not obvious if broad layers in the population are not positioned to technically receive it as a means of payment (e.g., not owning a computer or smartphone). Legally, it may not be possible either, because the creditor without access to the technology cannot accept the payment even if she wants to.

Anyways, this is the definition I’ve been applying to my real-time tabulation of retail CBDC explorers, but I frequently get suggestions to add new entries that don’t fit my definition. However, many turn out to be clearly wholesale CBDC, which are easy to identify and reject. And there are several more subtle ones that pop up, such as the Republic of Marshall Islands (RMI) SOV, and Cambodia’s Project Bakong, that I will briefly run through here. The SOV is easy to reject because there is no RMI monetary authority, and it is not denominated in the country’s unit of account, which is the U.S. dollar.

Cambodia’s Project Bakong has been sometimes called a quasi-form of CBDC but from my read of the white paper, it is arguably at most some form of synthetic retail CBDC. To me it appears to be a central bank-run interbank retail payments system that runs on distributed ledger technology rails that requires that any user balances be parked at the central bank. That makes it possibly a synthetic CBDC, in the same way that China’s AliPay and WeChat Pay are because they are required to park user funds at the People’s Bank of China. But in all these cases, the digital currencies are not issued by and direct liabilities of the central banks, so they’re not CBDC.

And the National Bank of Cambodia’s Chey Serey would seem to agree that Bakong isn’t a CBDC. “Instead, the platform augments the existing Fast and Secure Transfer (FAST), real-time retail payment system and Cambodian Shared Switch (CSS) that facilitate mainly interbank transactions among commercial banks and MFIs. They were launched respectively in 2016 and 2017 and are Cambodian riel (KHR) and US dollar account-based systems that do not interoperate with the twenty or so PSPs that serve mainly the unbanked. With the launch of Bakong, banks, MFIs and PSPs have a ready-made universal mobile app interface to connect users with FAST, CSS and each other.”

However, I have been long maintaining the Banco Central del Ecuador’s Dinero Electrónico mobile payment system in my CBDC explorer tabulation but being somewhat uneasy about its inclusion. The program, which operated between 2014 and 2018, allowed citizens to transfer USD balances in real-time from person to person using basic cell phones. From my read of a recent paper on the Dinero Electrónico it would seem to be a central bank-run USD asset-backed stablecoin. Like with the RMI, the USD is the country’s unit of account, but in this case the digital currency is indeed denominated in Ecuador’s unit of account, and it was issued by, and a liability of, the central bank. Hence, it’s a CBDC by my definition.

However, Marcelo Prates has suggested that digital currencies like the Dinero Electrónico is nothing more than a stablecoin issued by a central bank. Basically if the central bank can’t issue traditional money (reserves + cash), it can’t issue the “digital” version of this money. Hence, by this logic, only central banks that issue their own currency can issue CBDC, which precludes completely dollarized country central banks from issuing CBDC. Besides U.S. territories, these include Ecuador, El Salvador, Marshall Islands, Micronesia, Palau, Panama, Timor-Leste, and Zimbabwe. The same would go for countries in the eurozone and other currency unions. But would countries with currencies anchored to another country’s would still be able to issue CBDC?

BTW some might note that I don’t include in my tabulation the Avant smart card system created by the Bank of Finland in the 1990’s that was the world’s first CBDC. It is indeed a CBDC, but my tabulation seeks to cover CBDC projects that are potentially still live, whereas Avant shut down in 2006. However, I have added a new section to my tabulation for retail CBDC projects that have been shut down.

In that regard, I’m tempted to drop the Banco Central del Ecuador’s Dinero Electrónico from my CBDC explorer tabulation because it is now similarly defunct, and it is questionable whether the Ecuador central bank can even issue a CBDC. But alternatively, I could include the Avant as a CBDC that has launched/ piloted. Any thoughts out there?

Tabulated below are all of the central bank and sovereign retail digital currency launches and pilots I know of that have revealed their technology partners and platforms. I didn’t include the South Korean pilot because they haven’t revealed their technology partners or platforms. Please keep in mind that this is just a first crack and comments and suggestions are welcome.

I’ve tabulated the key features of the two active central bank digital currency (#CBDC) projects in the Caribbean area. The Central Bank of the Bahamas (CBOB) went live with its Sand Dollar on October 21, 2020 after a ten month pilot, and the Eastern Caribbean Central Bank (ECCB) started a twelve month pilot of its DCash on March 31, 2021 on four of the eight island countries under its currency union. This is all based on publicly-available information – hence some of the question marks. If there are errors of omission or commission, please let me know in the comments! Also, see below for an updated version of the PDF version of the table that includes the Central Bank of Uruguay 2017-2018 e-Peso pilot.

System utilizes enhanced short-lived one-time web tokens

?

Access

Smartphone & smart card

Smartphone only?

Transaction fees

Initially no, but maybe yes later

None during pilot

Interest bearing?

No

No

User tiers

Tier 1 requirements

Physical/email address, phone number and photo.

For “value-based“: Physical/email address, birth date/ place, phone number and photo.

Tier 1 transaction limit

B$1,500/month

EC$1,000/m or EC$2,700/m

Tier 1 holding limit

B$500

n/a

Tier 2 requirements

Tier 1 requirements plus govt.-issued photo identification

For “register-based“: Full name, address, phone number, and bank account

Tier 2 transaction limit

B$10,000/m

EC$3,000, EC$5,000, EC$20,000/d depending on risk profile

Tier 2 holding limit

B$8,000

n/a

High-value/business

Requirements

Business license & VAT ID number

Business name, physical/email address, phone number

Transaction limit

B$20,000/m or 1/8th of annual revenues whichever is greater.

EC$25,000/d to EC$300,000/d based on risk rating

Holding limit

B$8,000 or 1/20th of annual sales, up to an annual limit B$1 million.

n/a

Offline?

Users can make a pre-set dollar value of payments when communications access to the Sand Dollar Network is disrupted. Wallets would update against the network once communications were re-established.

The party initiating the transfer (sender) must have an internet connection. If the receiver is offline the payment will still be processed, and they will see the change in their balance as soon as they are back online.

Anonymity/Privacy?

Transaction transparency to enable central bank monitor suspicious transactions and stop accounts. Pseudonyms ensure user anonymity. Central bank maintains ledger and server is encrypted

Central bank can see anonymized transaction data and outstanding stock of DCash in each digital wallet. Registered financial institutions can fully observe the identity of payers and payees and the purpose of transactions

There is a growing queue of crypto-asset exchange-traded fund (ETF) applications at the U.S. Securities and Exchange Commission (SEC). So far, the SEC hasn’t been friendly towards the concept, pointing to inadequate means to prevent market manipulation and illicit activities at the top exchanges, as it rejected Bitcoin (BTC) ETF applications starting in 2018.

With institutional and retail crypto-asset investment interest surging, three firms (Valkyrie Digital Assets, Vaneck, New York Digital Investment Group) have recently submitted BTC-based ETF filings with the SEC. However, the approval process will be a long slog, with late September being a best guess as to when it will be complete, if successful. Hopes are high this time around because of the new Presidential Administration and the possibility of longtime crypto advocate Gary Gensler as SEC chair.

Meanwhile, the Ontario Securities Commission (OSC) cleared the launch of the Purpose Bitcoin ETF, making it the first publicly-traded ETF to gain regulatory approval in North America. After about a week of trading on the Toronto Stock Exchange it had bought 10,064 Bitcoin (about $450 million at a BTC price of $45,000). Soon after, the OSC approved the Evolve Bitcoin ETF but it appears to be off to a slower start. Also, CI Global Asset Manager filed a preliminary prospectus for its CI Galaxy Bitcoin ETF.

Alternatively, there is the Grayscale Bitcoin Trust and other similar closed-end trust products coming down the pipeline. Osprey Fund’s Bitcoin Trust is now available on a private-placement basis to retail investors. Bitwise Asset Management is seeking Financial Industry Regulatory Authority approval to trade shares of its Bitwise Bitcoin Fund on New York-based OTCQX over-the-counter (OTC) marketplace. BlockFi registered its new Bitcoin Trust with the SEC late last month. Bitwise launched a DeFi Crypto Index Fund that will track companies and securities involved in decentralized finance (DeFi).

Also, tech company MicroStrategy has been selling zero-coupon convertible senior notes with the intention to use the net proceeds to buy BTC. In December 2020 they sold $650 million of notes, and then another $1,050 million in February. However, a Gartner Finance poll of finance managers found that a majority of them are not planning to hold BTC as a corporate asset. In their responses, most of the 77 finance leaders interviewed cited BTC’s volatility as “extremely difficult to mitigate.”

The last Monthly Monitor talked about how USD-pegged Empty Set Dollar (ESD) briefly held the #6 position in the stablecoin league table. The ESD launched in September 2020 and was one of the first algorithmic stablecoins to come to market. (An algorithmic stablecoin adjusts its supply to maintain its peg.) However, ESD broke its peg massively in January 2021, and is now trading down around $0.13 resulting in a drop down to #14.

However, there’s another very viable-looking USD-pegged stablecoin, TerraUSD which sits at #7 ($590 million market capitalization). The peg isn’t absolutely perfect, as it has occasionally spiked down to nearly $0.96 and up to $1.04, but since it has launched in October 2019 it has spent most of its time within a $0.98 – $1.02 band, which is better than any other algorithmic USD-pegged stablecoin I’ve seen. TerraUSD is also part of the Terra family of products that seem to be seeing real use cases (see below).

Terra is a delegated proof of stake system that uses the LUNA token as collateral for the stablecoins it issues, and it has several active use cases underway:

The South Korean CHAI decentralized app-based mobile payments system runs on Terra’s payment rail. The rail is built on two the native stablecoin of Terra for funds across the networks and the Luna token for small transaction fees for miners. CHAI has partnered with 15+ major local banks to facilitate convenient fiat on/off ramps, recently crossed 2 million monthly active users. Terra’s network also integrates with MemePay, a Mongolian e-wallet utilized by 1.5% of the online population.

Terra’s Mirror synthetic assets protocol tracks the price of U.S. stocks, futures, exchange-traded funds, and other traditional assets. The Mirror Wallet kicked off with 12 of the top American technology stocks. The target market is users outside of the United States who seek 24/7 exposure to and fractional ownership of synthetic assets.

FYI besides TerraUSD there are eleven other Terra-based stablecoins (AUD, CAD, CHF, CNY, EUR, GBP, INR, JPY, HKD, KRW, and SGD).

{kind=link}